IQ-EQ Fund Performance Snapshot

The second quarter of 2026 delivered a remarkable recovery in global equities, with the MSCI World Index returning +14.6% on a total return basis over the period. The quarter was defined by two dominant and at times competing forces: the escalating and then de-escalating military conflict between the US and Iran, and a powerful AI-driven technology rally that ultimately proved resilient enough to carry global markets to their best quarterly performance since 2020. Regional equity benchmarks all posted strong gains, with the Nikkei 225 leading developed markets at +37.3%, the Euro Stoxx 50 at +15.6%, followed by the S&P 500 at +15.2%.

The conflict's trajectory through the quarter can be broadly divided into three phases: acute disruption (April–early May), partial restoration attempts (mid-May to mid-June), and de-escalation following the interim US–Iran peace deal announced on 14 June. By quarter-end, Brent had collapsed to $72.92/bbl — a decline of approximately 38% over the three-month-period — as the Hormuz reopening and anticipated supply normalisation overwhelmed the market.

The Information Technology sector was the standout performer, driven higher by renewed enthusiasm for the AI trade. The sector was responsible for over 60% of the total equity return during the quarter, rising by 34.8% in euro terms. Shares in companies such as Micron, Nvidia, AMD, Apple and Intel drove the sector higher.

The MSCI World Industrials sector returned +14.5%, supported by a surge in defence-related spending commitments across NATO members and a broader rearmament theme, though individual defence names were mixed — traditional companies such as Lockheed Martin, Northrop Grumman and Rheinmetall underperformed, while newer entrants and drone-focused companies attracted significant investor interest.

The Energy sector was the only sector to post a negative return during the quarter, having peaked on 31 March, one month after the US and Israel bombed Iran, sparking the conflict. By quarter-end the sector had lost all those gains as the oil price fell back to pre-crisis levels on expectations of the reopening of the Strait of Hormuz.

At IQ-EQ Fund Management, we focus on profitable businesses which generate persistent returns and have high levels of protection combined with competent management. We define these as quality businesses, and we expect them to perform irrespective of market volatility. In the long run, we believe these characteristics will deliver outperformance for our clients.

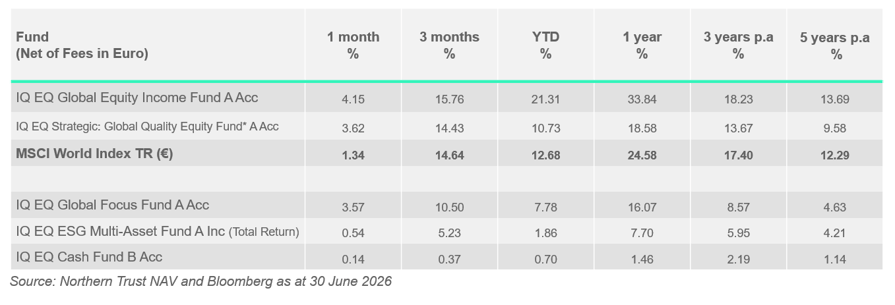

June 2026 figures for the IQ-EQ range of Funds:

IQ EQ Global Equity Income Fund: YTD 21.31% (Net of fees)

The IQ EQ Global Equity Income Fund returned +15.76% during the quarter, compared with the MSCI World Index, which rose by 14.64%. Stock Selection was a positive contributor to relative performance during the quarter, while Sector Selection was a slight negative. Currency Effects were minimal during the quarter. The Sector Selection outcome was driven by an underweight position in the Information Technology sector and an overweight position in Utilities. Industrials and an underweight position in the Consumer Discretionary sector. The underweight position in the Energy sector was a positive contributor to relative performance. Corning and TSMC were among the strongest contributors to equity performance during the quarter, while Zoetis and Telus were laggards.

Key contributors during the period include:

+ Corning Inc. (GLW) is a global technology-based company producing optical fibre, cable, and photonic components for the telecommunications industry, as well as manufacturing glass panels, liquid crystal display glass, and projection video lens assemblies for the information display industry. GLW has several secular opportunities which outweigh the cyclical exposures that many manufacturing companies face. The company has also noted strong demand more generally for US made components and equipment considering the new US tariff regime. Meanwhile, the company is executing on its strategic plan (“Springboard”), which had aimed to get operating margins to 20%, well ahead of schedule. GLW has been citing strong demand in its Optical division from AI-related business in recent quarters and announced in January that it had signed a deal to supply $6bn worth of optical products to Facebook parent Meta. The shares rose strongly on the news. Despite releasing an earnings update that disappointed some investors in May, the company is benefiting hugely from AI infrastructure investment. The shares rose sharply in early May after Nvidia announced a $500 million investment and a multiyear partnership to expand US optical connectivity manufacturing capacity tenfold. The company was among the best performers in the portfolio during the quarter.

+ Taiwan Semiconductor Manufacturing Company (TSM) is a multinational semiconductor production and development company headquartered in Hsinchu, Taiwan. TSM manufactures semiconductors for corporations such as Apple, Nvidia, AMD and Qualcomm. The company has become the dominant global microchip manufacturer due to its adoption of the “pure-play foundry” model, allowing it to focus on making chips that other companies design. TSM has become the primary chip supplier to the “Magnificent 7”. Despite ongoing concerns about tariffs and American relations with China, the company has confirmed that it will increase investment in the current year. TSM has excellent sustainability credentials, operating with an exceptionally strong competitive moat, allowing it to pay 70% of free cash flow in dividends each year. On 16 April, TSM released Q1 2026 results, reporting net revenue of NT$1.13 trillion, up 35% YoY, and net income up 58% YoY, with Q2 revenue guidance of $39.0–$40.2 billion beating analyst consensus. TSM's entrenched position in leading-edge semiconductor manufacturing, underpinned by structural AI demand that continues to outstrip supply, supports a constructive long-term outlook for the stock.

- Zoetis Inc (ZTS) is a global leader in animal health, developing and manufacturing medicines, vaccines, and diagnostic products for livestock and companion animals. The company operates across multiple therapeutic areas including parasiticides, dermatology, pain management, and diagnostics. Zoetis experienced a sharp deterioration in its outlook in the second quarter following disappointing Q1 results. On May 7, the company reported Q1 2026 revenue of $2.26 billion, up 3% YoY but below the $2.30 billion that investors had expected. The company cut its full-year 2026 guidance, lowering its adjusted EPS expectations to $6.85 to $7.00 from $7.00 to $7.10 and reducing revenue outlook to $9.68 billion. The reason for the downbeat outlook was intensifying competition in companion animal franchises. Zoetis has a significant range of products in development, which should drive growth in the future. However, the near-term EPS downgrades drove sentiment during the second quarter.

- Telus (T) is a Canadian telecommunications company providing wireless and wireline connectivity, internet, and television services, alongside healthcare and digital solutions through its Telus Health and Telus Digital divisions. In 2026, the company entered the year facing intensifying competitive pressures in the Canadian wireless market, with shares declining approximately 16% year-to-date by the close of the second quarter. On 8 May, Telus released Q1 2026 results, reporting adjusted EPS of C$0.23, beating the consensus estimate of C$0.22, though operating revenues of C$5.01 billion fell 0.9% YoY and missed expectations, with elevated churn remaining a concern; the company also announced a CFO transition, with Gopi Chande named as successor to Doug French. Despite the EPS beat and improving credit outlook, persistent investor concern over competitive intensity, elevated leverage, and dividend sustainability weighed on the shares.

Top 5: Corning Inc, TSMC, Intel, Samsung, Cummins.

Bottom 5: Zoetis, Telus, Waste Management, Pepsico, Swisscom.

IQ EQ Strategic: Global Quality Equity Fund*: YTD 10.73% (Net of fees)

The IQ EQ Strategic: Global Quality Equity Fund returned 14.43% over the quarter, compared with the MSCI World Index, which returned 14.64%. The Fund's underperformance was driven by Stock Selection, while Sector Allocation provided a positive contribution. Currency Effects were negligible. The positive Sector Allocation outturn was driven primarily by sector underweight positioning in Energy and overweight positioning in Information Technology. The Fund’s worst performing sector allocation was overweight positioning in Health Care. The negative contribution from Stock Selection was due to the poor performance of stocks such as Zoetis Inc and Accenture PLC.

Key contributors during the period include:

+ KLA Corp (KLAC) is the global leader in process control equipment for semiconductor manufacturing. The Company offers surface profilers, nanomechanical testers, chips, and semiconductor assembly solutions. Semiconductor Process Control, including wafer inspection, is the top revenue generating product line. The company's equipment is essential for manufacturing advanced semiconductors at 2-nanometer and 1-nanometer nodes. Q2 fiscal 2026 earnings delivered revenues of $3.3 billion and record free cash flow. This was driven by continued investment in foundry/logic and strength in DRAM/HBM. Management projects high-teens percentage year on year revenue growth in calendar 2026. Near-term challenges include supply constraints for optical components until mid-2026 and geopolitical tensions with China. KLA remains well-positioned to achieve its long-term revenue and operating margin targets, driven by increasing chip complexity and its leading market share in process-control equipment for AI chips.

+ Alphabet Inc. (GOOGL) is the parent company of Google, operating across search, advertising, cloud computing, and AI, including YouTube and Google Cloud. Digital advertising is its primary revenue source, with Google Cloud a fast-growing contributor. GOOGL entered the year with strong momentum, up approximately 23% year-to-date by early May. In April, Alphabet reported Q1 2026 results well ahead of expectations —revenue of $109.9 billion (+19% YoY), GAAP EPS of $5.11 versus consensus of $2.73, and Google Cloud up 63% YoY — lifting the stock approximately 10%. In early June, an $84.75 billion equity raise to fund AI spending weighed on the shares, though GOOGL still closed the quarter up approximately 24%. Management guided FY 2026 capex to $180–$190 billion, with 2027 spending expected to increase significantly. Alphabet's AI positioning and a Google Cloud backlog that nearly doubled QoQ to over $460 billion support a constructive long-term outlook.

- Zoetis Inc (ZTS) is a global leader in animal health, developing and manufacturing medicines, vaccines, and diagnostic products for livestock and companion animals. The company operates across multiple therapeutic areas including parasiticides, dermatology, pain management, and diagnostics. Zoetis experienced a sharp deterioration in its outlook in the second quarter following disappointing Q1 results. On May 7, the company reported Q1 2026 revenue of $2.26 billion, up 3% YoY but below the $2.30 billion that investors had expected. The company cut its full-year 2026 guidance, lowering its adjusted EPS expectations to $6.85-$7.00 from $7.00-$7.10 and reducing revenue outlook to $9.68 billion. The reason for the downbeat outlook was intensifying competition in companion animal franchises. Zoetis has a significant range of products in development, which should drive growth in the future. However, the near-term EPS downgrades drove sentiment during the second quarter.

- Accenture Plc (ACN) is a global professional services company providing strategy, consulting, technology, and operations services across a broad range of industries. It serves clients in more than 120 countries, with revenues split between consulting and managed services. Accenture’s shares were down 37% over Q2. In June, Accenture reported Q3 FY26 results. While adjusted EPS of $3.80 beat consensus of $3.71, revenue of $18.72B missed estimates and new bookings fell 2% YoY to $19.3B, sending shares down as much as 19% intraday. Management cited approximately $100 million in lost revenue from the Middle East conflict and slower client decision-making as key headwinds. Management narrowed FY26 revenue growth guidance to 3%–4%, trimming the prior top end of 5%. Analysts cut price targets sharply following the results, reflecting concern that AI disruption poses a structural threat to consulting demand. Despite a difficult quarter, Accenture's scale, advisory expertise, and significant AI investment, position it as a potential long-term beneficiary of enterprise AI adoption, with a $7.5 billion buyback programme and a record forty-one clients booking above $100 million quarterly signalling underlying confidence in the business.

Top Five: KLA Corp, Alphabet Inc, Lam Research, Tokyo Electron, Applied Materials.

Bottom Five: Accenture, Zoetis, Autodesk, Wheaton Precious Metals, Mastercard.

IQ EQ Global Focus Fund: YTD 7.78% (Net of fees)

The IQ EQ Global Focus Fund returned +10.50% during the quarter. The equity portfolio returned 15.7%, while the bond portfolio returned +1.0%. Within the equity book, TSMC and Cummins were among the best performers, while the biggest detractors from performance included Adobe and ADP. An overweight position in Industrials contributed positively to returns within the equity book.

Key contributors during the period include:

+ Taiwan Semiconductor Manufacturing Company (TSM) is a multinational semiconductor production and development company headquartered in Hsinchu, Taiwan. TSM manufactures semiconductors for corporations such as Apple, Nvidia, AMD and Qualcomm. The company has become the dominant global microchip manufacturer due to its adoption of the “pure-play foundry” model, allowing it to focus on making chips that other companies design. TSM has become the primary chip supplier to the “Magnificent 7”. Despite ongoing concerns about tariffs and American relations with China, the company has confirmed that it will increase investment in the current year. TSM has excellent sustainability credentials, operating with an exceptionally strong competitive moat, allowing it to pay 70% of free cash flow in dividends each year. On April 16th, TSM released Q1 2026 results, reporting net revenue of NT$1.13 trillion, up 35% YoY, and net income up 58% YoY, with Q2 revenue guidance of $39.0–$40.2 billion beating analyst consensus. TSM's entrenched position in leading-edge semiconductor manufacturing, underpinned by structural AI demand that continues to outstrip supply, supports a constructive long-term outlook for the stock.

+ Cummins Inc. (CMI) is a global power solutions provider that designs, manufactures, distributes, and services a range of engines, powertrain components, power generation systems, and electrified power systems, with operations in approximately 190 countries and territories. The company reports across five segments: Engine, Components, Distribution, Power Systems, and Accelera. In 2026, CMI entered the year with strong momentum, underpinned by record Power Systems profitability and robust data-centre demand, though initial guidance implied margin headwinds across several segments. CMI shares advanced 32.6% over Q2 2026, rising from $538 to $713, supported by strong earnings beat and a series of positive catalysts throughout the quarter. On 5 May, CMI reported Q1 2026 adjusted EPS of $6.15, beating consensus by approximately 10%, with net sales of $8.40 billion up 2.7% YoY; the company simultaneously raised its FY2026 revenue guidance to growth of 8% to 11%.

- Zoetis Inc (ZTS) is a global leader in animal health, developing and manufacturing medicines, vaccines, and diagnostic products for livestock and companion animals. The company operates across multiple therapeutic areas including parasiticides, dermatology, pain management, and diagnostics. Zoetis experienced a sharp deterioration in its outlook in the second quarter following disappointing Q1 results. On May 7, the company reported Q1 2026 revenue of $2.26 billion, up 3% YoY but below the $2.30 billion that investors had expected. The company cut its full-year 2026 guidance, lowering its adjusted EPS expectations to $6.85-$7.00 from $7.00-$7.10 and reducing revenue outlook to $9.68 billion. The reason for the downbeat outlook was intensifying competition in companion animal franchises. Zoetis has a significant range of products in development, which should drive growth in the future. However, the near-term EPS downgrades drove sentiment during the second quarter.

- Tractor Supply Company (TSCO) is the largest rural lifestyle retailer in the United States, operating a network of farm and ranch stores serving recreational farmers, ranchers, and rural homeowners. The company offers a broad assortment of products spanning livestock and pet supplies, hardware, tools, seasonal merchandise, and clothing. In 2026, the shares have faced significant headwinds reflecting persistent weakness in the companion animal category and a challenging consumer backdrop. Early in the quarter, analyst downgrades and price target reductions ahead of earnings weighed on sentiment; on 21 April, TSCO reported Q1 2026 results that missed expectations, with EPS of $0.31 against a $0.34 estimate and comparable sales growth of just 0.5% versus the 1.62% consensus, as pet segment softness and a multiyear-low operating margin of 6.5% drove the stock sharply lower on the day.

Top Five: TSMC, Cummins, ABB, Corning, Fanuc.

Bottom Five: Zoetis, Tractor Supply, Broadcom, Verizon, Swisscom.

IQ EQ ESG Multi-Asset Fund: YTD 3.26% (Total Return, net of fees)

Within the Equity Portfolio:

The IQ EQ ESG Multi-Asset Fund returned 5.23%, net of fees, during the quarter. The equity component, which accounts for ca. 61% of the strategy, returned 8.55% gross. This compares with the MSCI World Index return of 14.64%. The relative performance of the equity book was driven mainly by negative Stock Selection. Currency Effects and Sector Allocation decisions were marginally negative. The Stock Selection outcome was almost entirely due to the Information Technology sector, particularly semiconductor makers such as Micron and Nvidia and AMD, which are not owned in the portfolio – Micron, alone, was responsible for 1.2% of the total underperformance. Sector Allocation was positively impacted by the underweight in Energy stocks, which counteracted the negative underweight position in Information Technology stocks.

Key contributors during the period include:

+ Taiwan Semiconductor Manufacturing Company (TSM) is a multinational semiconductor production and development company headquartered in Hsinchu, Taiwan. TSM manufactures semiconductors for corporations such as Apple, Nvidia, AMD and Qualcomm. The company has become the dominant global microchip manufacturer due to its adoption of the “pure-play foundry” model, allowing it to focus on making chips that other companies design. TSM has become the primary chip supplier to the “Magnificent 7”. Despite ongoing concerns about tariffs and American relations with China, the company has confirmed that it will increase investment in the current year. TSM has excellent sustainability credentials, operating with an exceptionally strong competitive moat, allowing it to pay 70% of free cash flow in dividends each year. On April 16th, TSM released Q1 2026 results, reporting net revenue of NT$1.13 trillion, up 35% YoY, and net income up 58% YoY, with Q2 revenue guidance of $39.0–$40.2 billion beating analyst consensus. TSM's entrenched position in leading-edge semiconductor manufacturing, underpinned by structural AI demand that continues to outstrip supply, supports a constructive long-term outlook for the stock.

- Tractor Supply Company (TSCO) is the largest rural lifestyle retailer in the United States, operating a network of farm and ranch stores serving recreational farmers, ranchers, and rural homeowners. The company offers a broad assortment of products spanning livestock and pet supplies, hardware, tools, seasonal merchandise, and clothing. In 2026, the shares have faced significant headwinds reflecting persistent weakness in the companion animal category and a challenging consumer backdrop. Early in the quarter, analyst downgrades and price target reductions ahead of earnings weighed on sentiment; on April 21st, TSCO reported Q1 2026 results that missed expectations, with EPS of $0.31 against a $0.34 estimate and comparable sales growth of just 0.5% versus the 1.62% consensus, as pet segment softness and a multiyear-low operating margin of 6.5% drove the stock sharply lower on the day.

Within the Bond Portfolio:

Performance

The bond portfolio was up 1.04% during the second quarter, outperforming its benchmark, the JP Morgan Global Bond Index (unhedged in euros), which was up 0.96%. Regarding relative performance, the main positive contribution came from the portfolio’s allocation to non-benchmark government, government agency and corporate bonds which outperformed as spreads tightened. This was offset somewhat by an overweight position in long dated Japanese Government Bonds funded out of an underweight in long dated US Treasuries. This underperformed as the Japanese government surprised the market by announcing a long-term strategy to raise investment in key industries, which is likely to increase borrowing and bond issuance in future years.

Top Five: TSMC, Alphabet, Siemens, Singapore Exchange, State Street

Bottom Five: Tractor Supply, Zoetis, EssilorLuxottica, PepsiCo, TJX Companies

IQ EQ Cash Fund: YTD 0.70% (Net of fees)

The gross running yield on the Cash fund at the end of the second quarter of 2026 was 2.02% as the European Central Bank (ECB) continue to monitor inflation, European infrastructure spending as well as the impact of geopolitical events such as the Middle East to the current cycle of monetary policy. The Fund Management team continues to maintain ca. 30% of the fund in short term liquidity & short-dated government bonds, blended with deposits termed out for different maturities out to a maximum of one year.

The ECB raised interest rates in June for the first time since 2023, citing the inflationary pressures of the conflict in the Middle East as officials announced the 0.25% expected move. The accompanying statement showed officials believe that the outlook remains uncertain, with upside risks for inflation and downside risks for economic growth and that the full implications of the war for medium-term inflation and growth will depend on the intensity and duration of the energy price shock, as well as the scale of its indirect and second-round effects. ECB President Lagarde added that ‘the war in the Middle East is weighing on activity, and surveys are pointing to a slowdown, especially in services and the increase in energy prices will lift inflation further over the summer and keep it well above target into the first half of 2027’. While ECB Officials did not rule out another move in July, markets are leaning towards September for possible further monetary tightening. While the IMF warned that the policy rate will need to rise to keep the impact of the shock on inflation contained, it also noted that if the increase in inflation expectations is paired with substantial deterioration in financial conditions and lower demand, a more negative output gap would limit inflation pressures and reduce tightening needs.

European Central Bank (ECB) Governing Council member Kazaks said that the central bank does not need to raise interest rates a number of times in succession, adding that ‘the calming of the conflict reduces the risk of nonlinearities and second-round effects and gives us more time to see what happens with the economy and what the monetary policy response should be.’ Fellow Governing Council member Schnabel said that the central bank will most likely have to increase interest rates further in order to tame price pressures, stating that the ‘extent and timing of further measures will depend on how the conflict, the economy, and inflation evolve.’

Key contacts

If you have any queries please contact Timothy.Kelly@iqeq.com. or any member of our sales team at assetmanagement@iqeq.com. Additional information on the Davy Funds Plc range of funds can be found on our website here.

************************************************

WARNING: Past performance is not a reliable guide to future performance. The value of investments may fall as well as rise. Investments denominated in non-euro currencies, may be affected by changes in exchange rates when converted to euro or other currencies.

* Effective 1st May 2024 the IQ EQ Fund Management (Ireland) Limited managed sub-funds on the Davy Funds Plc umbrella were renamed removing “Davy” from the name and/or including “IQ EQ”. ( Davy Global Equity Income Fund to IQ EQ Equity Income Fund; Davy Strategic: Global Quality Equity Fund to IQ EQ Strategic: Global Quality Equity Fund; Davy Global Focus Fund to IQ EQ Global Focus Fund; Davy ESG Multi-Asset Fund to IQ EQ ESG Multi-Asset Fund, and Davy Cash Fund to IQ EQ Cash Fund). There has been no change to the investment objective or process.

IQ EQ Fund Management (Ireland) Limited is regulated by the Central Bank of Ireland. Details about the extent of our authorisation and regulation by the Central Bank of Ireland are available from us upon request.